In Part 7, I described the moment in June 2017 when I discovered a Valeo management presentation from April 2009—a document created three months before I first contacted the firm. This record didn’t just reveal a different business model; it revealed an existential survival strategy born from a culture of risk that Valeo never intended for me to see.

A Culture of Risk

To understand the decision-making at Valeo, it helps to understand the culture of the firm. It was an environment where high-stakes risks were not just professional, but social. One annual staff Christmas party, for instance, featured a “casino night” hosted by a partner, complete with professional blackjack tables and other gambling equipment.

This environment of risk-taking appeared to extend to their professional oversight. Years later, while the firm was arguably more focused on pursuing litigation against me than monitoring its own practice, management failed to notice that a younger advisor was in the process of embezzling $4.69 million from clients into a fake company to fund personal expenses and sports gambling.

In late 2008, as the global economy cratered, this culture of risk met a predictable reality.

The Squandered Warning

Valeo’s billing model is inherently predictable. Their client fees are fixed for four consecutive quarters based on the portfolio values on December 31st. Because the new billing cycle doesn’t start until April 1st, the firm has a built-in three-month advance warning on their likely revenues for the entire following year.

Had management applied even a basic level of professional diligence, the impending financial struggle for 2009 would have been undeniable as early as November 2008. Instead, the firm’s actions suggest they were not paying attention—or perhaps didn’t care enough to look. By December 31, 2008, the “cliff” was a certainty, yet management waited until the disastrous April 1st billing had already taken place to address it.

The Disconnect in Diligence

While Valeo management was waiting for a market rebound that never came, I was taking proactive steps to protect my small practice:

Operating Expenses: At the start of 2009, I terminated my office lease and moved into a home office in my basement, cutting every possible operating expense to the bare minimum.

Investment Strategy: In July 2008, I implemented an option strategy for my clients that limited possible losses to an amount they could live with. And they did.

Looking back at the emails I sent Valeo during my recruitment, I had no idea of the contrast between us. I was fearful of competing against them because they were paying for Google ads in my market and claiming they were ready for a “momentous” expansion.

In reality, Valeo was over-leveraged. They had contracted for an expensive new office in a prime development at 96th and Meridian Street—directly behind the high-traffic McDonald’s where travelers from Northern Indiana routinely stop on their way into downtown Indianapolis. They were moving into an anchor-tenant spot with the “Valeo” sign prominently displayed at the top of the building, just as their primary revenue stream was cratering.

The Saturday Meeting

On Saturday, April 18, 2009—seventeen days after the revenue reset—the Finance and Management Committees finally met to face the consequences of their lack of urgency:

The Revenue Crisis: Projected invoices for Q2 2009 were down 30% sequentially.

The Realized Decline: Realized revenues were actually down 67% from the prior quarter, dropping from $686,000 down to $226,000. While delayed billing entries may have eventually improved this, that was Valeo’s actual financial reality at that moment.

The Admission: Management noted that the “financial stress from downturn spotlights what we all knew but failed to address”.

The Directive: Their conclusion was blunt: “Without [performance standards] we cannot manage finances”.

The Solution: Employee Wage Fines

Having ignored the warning signs for months, the firm chose a survival mechanism that shifted the cost of their lack of diligence onto their employees. The April 2009 presentation codified the math of what they called “Performance compensation reductions”:

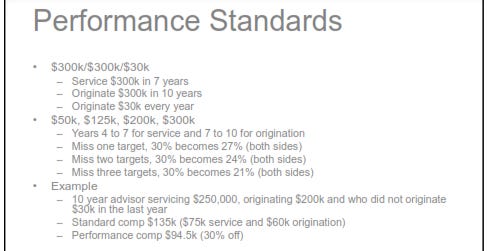

Missing revenue targets would trigger a reduction in an advisor’s compensation percentage—slashing pay from 30% of revenue generated and / or serviced down to 27%, 24%, or even 21%.

The document modeled an example where a senior advisor would be “fined” $40,500 (a 30% reduction) to bridge the firm’s revenue gap.

Management set the implementation date for all employees as January 1, 2010. Valeo had taken a bet on the market and lost. They had ignored the consequences until they were undeniable. And when reality finally hit, they chose to force their employees to pay for those consequences.

_______________________

Were those performance standards legal under Indiana law?

_______________________

In Part 9, we look at developments that suggest Valeo knowingly broke the law—leading to a timeline where demand letters, attorney invoices, and a sudden and timely change in that very law converged to provide a legal shield for this business model.

No comments:

Post a Comment